Mar 22, 2023

What Wall Street had to say about the U.S. Fed's rate hike

, Bloomberg News

Federal Reserve Caught Between Inflation and Banking Crisis

VIDEO SIGN OUT

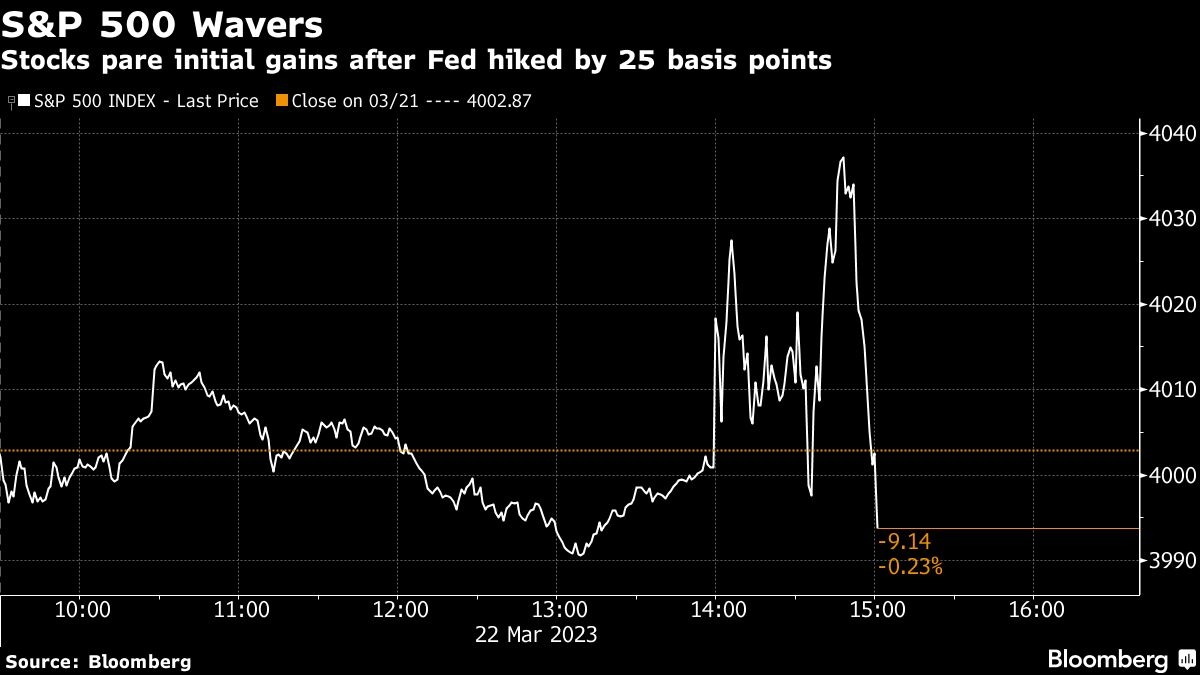

Wall Street widely expected the Federal Reserve to raise interest rates by 25 basis points, which is exactly what happened. But equity investors debated conflicting messages: the policy guidance shifted from “ongoing” rate increases to “some additional” policy firming, though Chair Jerome Powell said that the Fed’s hands aren’t tied.

Stocks gained in the immediate aftermath and then sank. Treasuries and the dollar fell. Investors pouring over the Fed’s Summary of Economic Projections didn’t get much help there, since the Fed’s expectations for unemployment and inflation were little changed.

While Chair Powell said in his news conference that the policymakers had weighed a pause in rate hikes ahead of their meeting, the Fed remained focused on the risks of high inflation even as it watched developments in the banking system. “If we need to raise rates higher, we will,” he said.

“This is about as hawkish as the Fed can be given the banking sector stresses that are ongoing,” said Win Thin, global head of currency strategy at BBH. “To me, the statement is similar to what the ECB said. That is, once we get past the banking sector stresses, the tightening cycle likely remains intact.”

Here’s what others on Wall Street had to say:

Sonia Meskin, head of US macro at BNY Mellon:

“This is slightly hawkish, yes, though the market so far appears to give it a dovish read, which possibly makes sense given that Powell’s most recent pronouncement before the blackout period opened the door to a 50 bps hike and a more material tightening that the March SEP actually reflects.”

Joe Gilbert, portfolio manager at Integrity Asset Management:

“Powell is trying to have it both ways. He is trying to appease both the hawks and the doves. This ultimately may be the last rate hike this year but Powell has to make the market believe that it isn’t because that would loosen financial conditions too much. The softening to come in the economy from the banking collapses has yet to be felt and the Fed knows this but they can not be alarmists.”

Seema Shah, chief global strategist at Principal Asset Management:

“The past roller coaster month has seen Powell go from dovish, to hawkish, and presumably back to dovish, with market expectations following this volatile ride. Policymakers will be desperately hopeful that inflation plays ball and the deceleration trend reasserts itself soon, validating today’s decision. If not, April and May could be potentially even more exhausting months.”

Matthew Hornbach, global head of macro strategy at Morgan Stanley, on Bloomberg TV:

“What strikes me is how they have balanced financial stability concerns against concerns about sticky inflation. The way they have done it is they have told us they are going to hike less but cut later. That seems like a pretty rational decision. I think the market should feel comfortable. The bond market is going to have a very difficult time taking out these rate cuts that are priced in through the balance of this year.”

Scott Ladner, chief investment officer at Horizon Investments:

“For as much consternation as there was about how the dots might change and the probable hike, this is a pretty on-the-screws event. They hiked the predicted 25bps, didn’t really change anything meaningful in the dots or SEP, and just lightly acknowledged that the banking stresses over the past two weeks may impact credit creation and therefor economic growth.”

Oscar Munoz, US Macro strategist at TD Securities:

“The SEP growth and UE rate projections were kept basically the same. That’s despite having a UE rate at 3.6 per cent now and Q1 growth running fairly strong in Q1. This means that they’re clearly expecting significant slowing before the end of the year and into 2024.”

Omair Sharif, founder of Inflation Insights:

“You’d only need two people to move up from 5.125 per cent for a half-hike and three to move up to get another full 25 bps. That doesn’t seem like a high bar given that we’ve got a long way to year-end and if the banking stress resolves soon enough, they may revert back to focusing more closely on inflation.”

“Add in the fact that the statement indicated that ‘some additional policy firming may be appropriate’ and I don’t think you want to bank on the fact that 5.1 per cent will be the terminal rate.”

Vincent Reinhart, chief economist at Dreyfus and Mellon:

“The basic question is should you deflect the path of policy from design purely for maximum employment and stable prices because of a concern about stability risks. Right now, I think Chair Powell isn’t accepting that as an argument, and really is adopting what I’ve always called the ‘separation principle,’ which is if you do banking supervision, regulation and crisis management, you have a freehanded monetary policy.”