Mar 16, 2022

Powell quiets stock cacophony by scoffing at U.S. recession talk

, Bloomberg News

Fed’s projected rate hikes won't be sufficient to control inflation: Former Fed official

VIDEO SIGN OUT

While history suggests it won’t last, an emotion approaching euphoria descended on equity markets Wednesday after Federal Reserve Chair Jerome Powell persuaded investors his first interest rate hikes in four years won’t throttle the economy.

Markets initially shuddered after the quarter-point increase was announced, but quickly found their footing as Powell made a point of repeatedly affirming the pace of economic growth. The Fed chief reported scant evidence of a downturn anytime soon, saying probability of a recession in the next year is “not particularly elevated.”

Indexes rebounded sharply in the aftermath, with the S&P 500 closing more than 2 per cent higher after briefly erasing gains as Powell began speaking. The Nasdaq 100 Index soared 3.7 per cent, the most in a year.

The buoyancy attests to how quickly the perception of threats has evolved in risk markets. Once, pronouncements of economic confidence were enough to shock stocks because of the cover they provide for rate hikes. Now such commentary is cause for celebration as anxiety about a recession becomes the larger concern.

“Jobs are stronger than ever. The unemployment rate is lower than pre-COVID, basically. Consumer spending is quite healthy. Consumer savings remains at all-time highs at US$2.7 trillion,” said Sylvia Jablonski, CEO and CIO of Defiance ETFs. “It’s really hard to think about how we would go into a recession.”

While not reflected in data or forecasts, recession angst has seeped deeply into trader psyches, and on some recent days has dominated them. Among signals bears are heeding are a worrisome flattening in the gap between short- and long-term interest rates, spiking oil prices that threaten demand and declines from stock records that recently exceeded 10 per cent in the S&P 500 and 20 per cent in the Nasdaq Composite Index.

No such anxiety was evident in the wake of Powell’s performance. Nine of 11 sectors in the S&P 500 finished Wednesday higher, with technology stocks outperforming even as Treasury yields climbed.

To be sure, Powell’s commentary wasn’t the only thing buttressing risk assets. Stocks soared overnight after China vowed to support its financial markets, giving a reprieve to beaten-down technology shares. Equities got a further boost from speculation Russia and Ukraine had moved closer to a compromise in peace talks.

It’s also not unusual for stocks to rally in the early stages of a tightening cycle. Among five Federal Open Market Committee meetings since 1990 when an initial rate hike was announced, four saw gains in the S&P 500. Often it was pronouncements about the economy’s health that spurred the advances.

Wednesday’s rebound in risk appetite lands in a market where conviction is lacking. The murkiness of the outlook for growth, inflation and interest rates -- as well as the war in Europe -- has translated into extreme swings in asset prices. Though it fell while Powell spoke, the Cboe Volatility Index has spent most of the last two weeks above 30, exceeding its historical average. Speculation that the Ukraine invasion would worsen inflation contributed to a stretch of futility that saw the S&P 500 slump in nine of 11 days through Monday.

In the eyes of Cetera Investment Management’s Gene Goldman, there’s more turbulence to come as policy makers navigate that landscape.

“The Fed is suffering from blissful ignorance,” said Goldman, the firm’s chief investment officer. “How can they expect to dramatically raise rates in the next two years -- I think 10 times for this year and next year in total -- but they don’t expect the unemployment rate to move higher, they expect economic growth to not be impacted that much?”

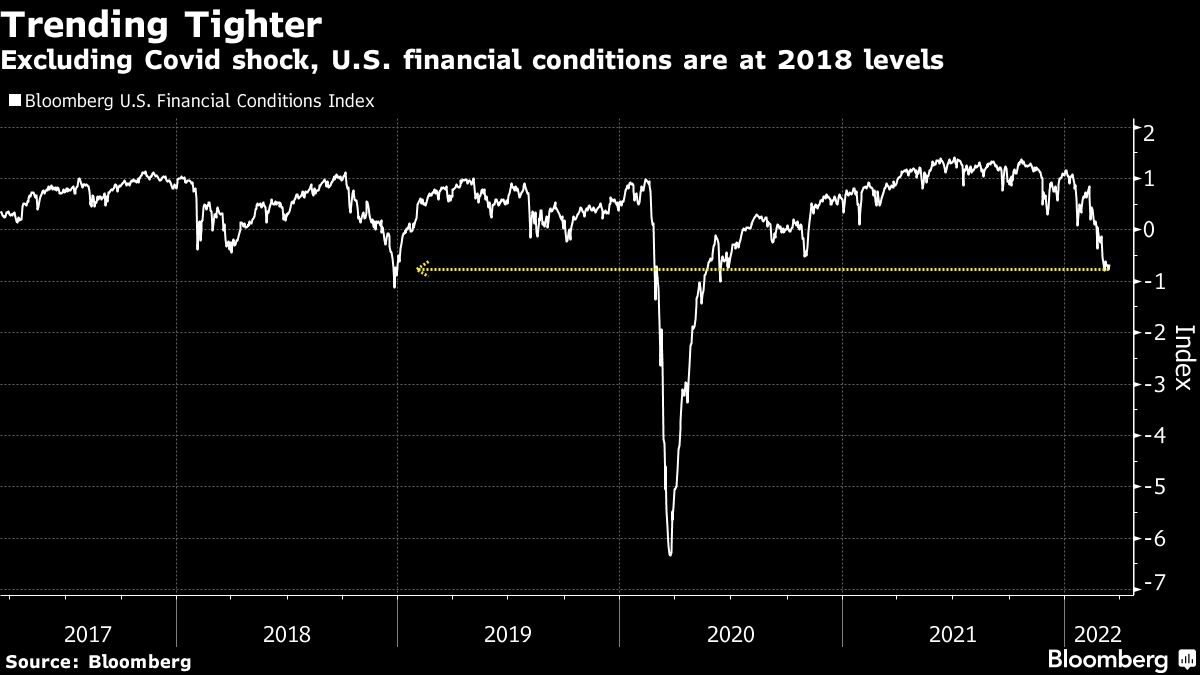

Powell indirectly addressed those concerns, noting that financial conditions “have already incorporated a significant number of rate increases.” Excluding the 2020 coronavirus shock, they sit near the tightest levels since 2018, according to the Bloomberg measure of U.S. financial conditions.

Financial conditions -- a multi-input measure of stress across equity and credit markets -- is how monetary policy changes are transmitted to the real economy, Powell said Wednesday. Continued tightening may allow the Fed to hike less overall, especially as the Fed begins to whittle down its massive balance sheet, according to Adam Phillips of EP Wealth Advisors.

“Financial conditions allowed the Fed to get away with a quarter-point hike today,” said Phillips, managing director of portfolio strategy at EP Wealth Advisors. “We learned today that the Fed could start shrinking the size of its balance sheet as early as May, so we will be interested to see how this amplifies the impact of policy tightening coming from higher rates.”