Housing costs, and Canada’s unique way of capturing them in inflation, suggest that consumer price gains may slow rapidly in coming months.

As the largest expense for most households, shelter makes up 30 per cent of Canada’s consumer price index — a similar proportion to the U.S. But unlike its southern neighbor, Canada’s inflation metrics capture these costs in a way that’s more sensitive to changes in interest rates and home prices.

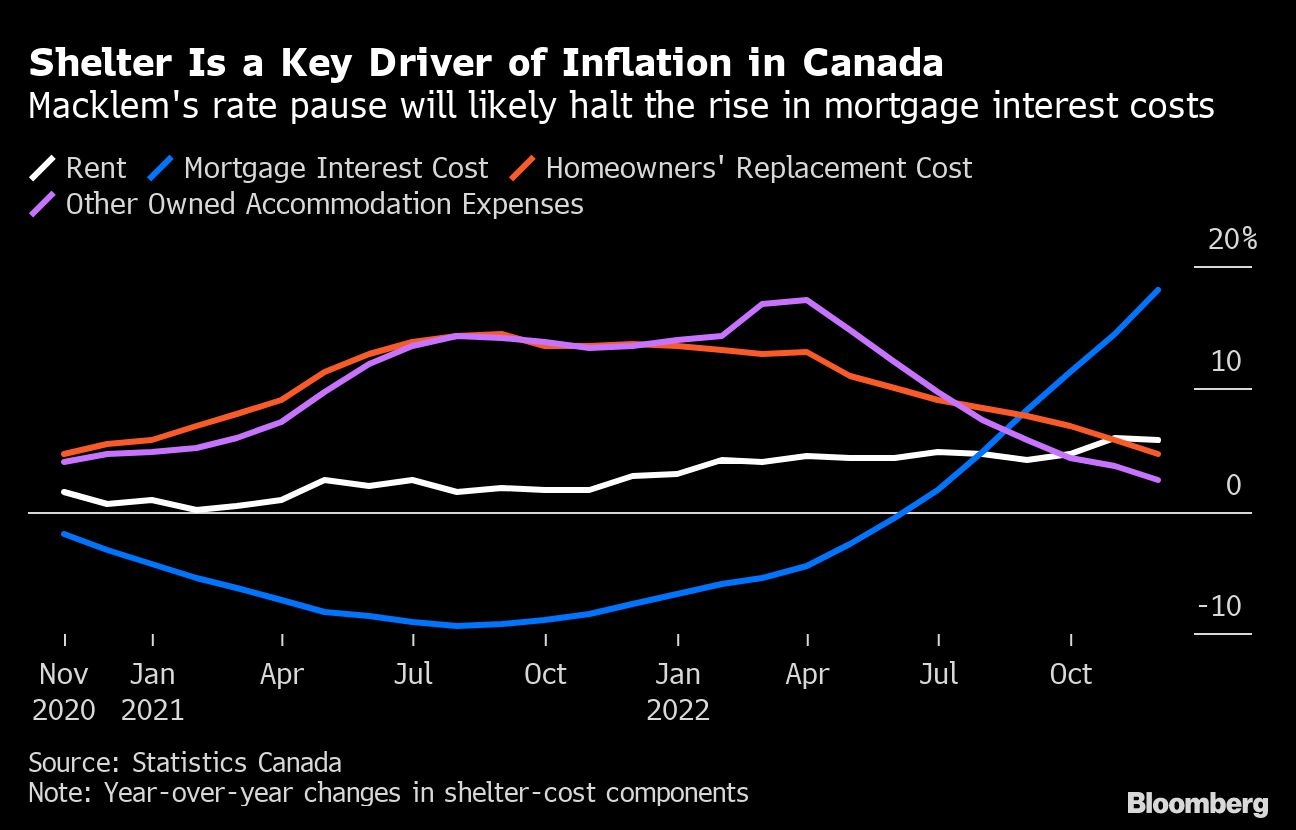

That means Canadian inflation measures are influenced by both the rise in mortgage costs as the Bank of Canada aggressively raises rates and by the resulting slowdown in the housing market.

While inflation was still 6.3 per cent in December, price pressures in Canada are expected to lose momentum thanks to base effects and continued cooling in the Canadian real estate market, which features shorter-duration mortgages than the U.S. and a higher share of variable-rate home loans.

Those differences are one reason economists say the Bank of Canada — which said this week it intends to pause its tightening campaign — won’t have to raise borrowing costs as high as the Federal Reserve.

“One way Canada actually stands out from a lot of other countries is that when the Bank of Canada raises interest rates, there’s a temporary boost to inflation because of this mortgage interest rate effect,” Stephen Brown, an economist at Capital Economics, said by phone.

CROSS-BORDER DIFFERENCES

The U.S. calculates housing inflation using owners’ equivalent rent, or the price a property owner would have to pay to rent to live there. Canada calculates it through a formula that includes mortgage interest, replacement cost, property taxes and maintenance.

Shelter has been a major driver of Canadian inflation in recent months, and was up 7 per cent in December. The mortgage interest and rent sub-indexes saw year-over-year jumps of 18 per cent and 5.8 per cent, respectively.

But with rates now on hold, Brown expects mortgage interest costs to peak before dropping sharply in the second half of this year. Other inflation inputs, such as commissions on home sales, are already easing.

His forecast is for increases in the shelter component of CPI to fall to 3.5 per cent by June and to 1.5 per cent by December. With energy, food and goods prices also expected to fall sharply, Brown said the Bank of Canada may be “underestimating how quickly overall inflation will decline.”

Macklem’s rapid interest-rate hikes, to 4.5 per cent from an emergency pandemic low of 0.25 per cent in March, have dramatically cooled the real estate market. Prices have fallen more than 13 per cent since their peak last year. Higher mortgage costs are also squeezing some of the world’s most indebted households, forcing them to tighten their purse strings.

“The bank might be feeling like they’ve done enough on housing, and that the effect is going to unravel over the coming months,” said Rishi Mishra, an analyst at Futures First Canada Inc. “They don’t want to press down too hard, just because how large the exposure is to housing market in Canada.”

Advertisement